Find your best local estate agent Start here

Remortgaging to release equity means you can free up cash you’ve built up in your home. But how do you do it, how much does it cost and what are the pros and cons? We take a look

When you remortgage, you take out a new mortgage deal on the same property. You may switch to a different lender or get a new mortgage with your current lender.

While one major reason to remortgage is switch onto a better deal when your current mortgage ends in order to save money, another reason for remortgaging is to release equity from you home. This means taking out a bigger loan against your property in order to free up some of the cash you’ve built up in it.

Remortgaging to release equity is very common; in fact the LMS Monthly Remortgage Snapshot showed that in March 2025, 47% of people who remortgaged increased their loan size, by an average of £20,224.

However, remortgaging to release equity means your debt will increase so it’s a good idea to weigh up the pros and cons and to get expert advice from a mortgage broker. Read on for more.

Equity is the proportion of your home that you own. There are two ways your equity can increase:

You can work out your home equity by taking away your outstanding mortgage balance and any outstanding secured loans from the value of your property.

For example, if your home is valued at £400,000 and you have £200,000 left to pay on your mortgage, the amount that’s left is your equity in the property – in this case £200,000.

There are lots of reasons why people remortgage to release equity, such as:

It’s important to note that remortgaging to release equity by taking out a bigger mortgage is different to equity release. Equity release is a way of releasing money from the value of your home if you’re over 55 without having to move out or pay it back during your lifetime. Read on for more on this.

Get fee-free remortgage advice from our partners at L&C. Use the online remortgage finder or speak to an advisor today.

Remortgaging to release equity involves taking out a new mortgage deal on your property that’s bigger than your current one.

So for example, if you owe £100,000 on your existing mortgage but take out a new mortgage for £130,000, you would get access to £30,000. But be sure to check any remortgaging costs you may need to pay, like an arrangement fee. Our partners at L&C can check your current mortgage terms and look for the best remortgage deal for you, searching over 90 lenders so you don’t have to. You can call them on 0800 0732326 to speak today or start the process online.

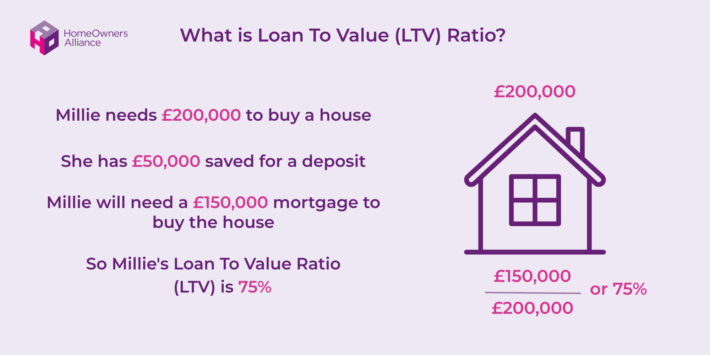

Your loan to value ratio tells you what proportion of your home is borrowed.

The lower your LTV, the better the mortgage rates you’ll usually get access to. So after 5 years, if the above house has increased in value to £250,000 what happens to your LTV?

If you remortgage to release equity your mortgage payments will be higher than if you remortage without releasing equity because your debt will be bigger. You’ll also pay more in interest over the term of the mortgage, so it’s a good idea to make overpayments on your mortgage if you can afford to and assuming your deal allows you to.

Also, if the amount of equity you release when remortgaging pushes you into a higher LTV band, you may have to pay a higher rate on your mortgage too.

Get fee-free remortgage advice from our partners at L&C. Use the online remortgage finder or speak to an advisor today.

You’ll need to weigh up the pros and cons of remortgaging to release equity:

Yes, you can take out a mortgage on a property you own outright to release equity from your home. This type of mortgage is called an unencumbered mortgage. It’s similar to a remortgage because you’ll be releasing equity from a property by borrowing money against its value, except an unencumbered mortgage is a in effect a brand new mortgage on the property.

To get an unencumbered mortgage, the first step is to get a Mortgage Agreement in Principle. This takes just 15 minutes to complete and can be done online now.

Arrange an Mortgage Decision in Principle today with the mortgage experts at L&C

There are different ways in which you may release equity so that you can buy another property:

Remortgaging to release equity may be worth considering if you have a decent chunk of equity in your home and are seeking to raise some money. But you’ll need to think carefully before increasing the size of your mortgage and what this means for your repayments.

Get fee-free remortgage advice from our partners at L&C. Use the online remortgage finder or speak to an advisor today.

There are some alternative options to remortgaging to release equity you may want to explore:

Equity release is a way of releasing money from the value of your home if you’re over 55 without having to move out or pay it back during your lifetime.

With a lifetime mortgage, you borrow money against the value of your property. The amount you can borrow depends on the value of the property and your age (and that of your partner if it’s a joint scheme).

While with a home reversion scheme, you can sell all or part of the property to a reversion provider. This means that, if your property increases in value and you sell up, you’ll only benefit from that increase on the part of the property you own.

In both cases, you’ll be allowed to stay in your home until you either die or go into long-term care, unless you breach the contract, such as by letting your home fall into disrepair. In those cases, technically, you could be forced to leave. Find out more in our guide Is equity release right for me?

Try Key Advice’s equity release calculator today to find out how much you could release

Releasing equity by remortgaging usually takes 4 to 8 weeks but it will vary depending on your circumstances.

Yes, you can move house if you remortgage. You’ll do this by either Porting your mortgage. This means moving your existing mortgage to your new property. Or by paying off your mortgage with the money you receive from your sale. And taking out a new mortgage on your new property. Although it’s important to check if you’ll need to pay fees like an Early repayment charge if you do this. Find out more in our guide Selling a house with a mortgage

When you remortgage there are a number of costs you may need to pay including those associated with your new deal such as arrangement fees, mortgage valuation fee and conveyancing fee. And you may need to pay fees to leave your current deal such as an exit fee and early repayment charge. Find out more in our guide Remortgaging costs: How much will you have to pay?

The amount of equity you can release will depend on your personal circumstances and your lender. It’s as good idea to get expert mortgage advice. Speak to fee-free mortgage brokers at L&C for advice on remortgaging to release equity.

Yes, you can release equity from your house by remortgaging. Or you may choose to release equity from your home by downsizing, which means selling up and buying a cheaper property. Once you’re over 55 you may decide to explore equity release options.

LTV stands for Loan to Value ratio and means the proportion of your home is borrowed. For example, if your home is worth £200,000 and has an outstanding mortgage balance of £150,000, your LTV is 75%. The lower your LTV the better rates you’ll usually get access to. The best mortgage rates are usually for those with a 60% LTV or lower.

HomeOwners Alliance Ltd is registered in England, company number 07861605. Information provided on HomeOwners Alliance is not intended as a recommendation or financial advice.

Mortgage service provided by London & Country Mortgages (L&C), Unit 26 (2.06), Newark Works, 2 Foundry Lane, Bath BA2 3GZ, authorised and regulated by the Financial Conduct Authority (FRN: 143002). The FCA does not regulate most Buy to Let mortgages. Your home or property may be repossessed if you do not keep up repayments on your mortgage.

HomeOwners Alliance Ltd is an Introducer Appointed Representative (IAR) of LifeSearch Limited, an Appointed Representative of LifeSearch Partners Ltd, authorised and regulated by the Financial Conduct Authority. (FRN: 656479).

Independent Financial Adviser service is provided by Unbiased, who match you to a fully regulated, independent financial adviser, with no charge to you for the referral.

Bridging Loan and specialist lending service provided by Chartwell Funding Limited, registered office 5 Badminton Court, Station Road, Yate, Bristol, BS37 5HZ, authorised and regulated by the Financial Conduct Authority (FRN: 458223). Your property may be repossessed if you do not keep up repayments on a mortgage or any debt secured on it.