Find your best local estate agent Start here

Remortgaging when your current deal ends could save you thousands of pounds a year. But should you fix? And for how long? What if your house value has increased? And with some of the best remortgage rates creeping up, when and how do you lock in to get the best deal?

Use the online mortgage finder to compare your current mortgage with other deals.

Get fee-free remortgage advice from our partners at L&C. Use the online remortgage finder or speak to an advisor today.

Yes. Remortgaging when your current deal ends could save you thousands of pounds a year on your mortgage payments. The amount you can save will depend on the rate on your current mortgage deal vs the mortgage rate you can get.

If you’re coming off a cheap fixed rate mortgage in 2025, your new mortgage is likely to cost you more every month than your current one. But remortgaging could still save you money because if you do nothing and end up on your lender’s standard variable rate it could cost you significantly more.

The average 5 year fixed rate mortgage in June 2020 was around 2.4%. By comparison, the average 5 year fixed rate mortgage in June 2025 is 4.66%.

Here’s an illustration of how much you’ll pay at these rates if you borrow £200,000 over 30 years.

| Mortgage payment at June 2020’s average rate 2.4% | Mortgage payment at June 2025’s 4.66% | How much more you’ll pay in June 2025 |

|---|---|---|

| £780 | £1,032 | £252 |

But if you do nothing and roll onto your lender’s standard variable rate (SVR), which average 7.60%, you’ll pay much more.

Here’s how much you’ll pay on a £200,000 mortgage over 30 years at 7.60%, compared to if you remortgage at June 2025’s average 5 year fix rate of 4.66%.

| Mortgage payment at June 2025’s average rate 4.66% | Mortgage payments on average SVR of 7.60% | How much more you’ll pay if you move to SVR |

|---|---|---|

| £1,032 | £1,412 | £380 |

If you’re coming off a 2 year fixed rate mortgage, the good news is that mortgage rates are now lower than 2 years ago. The average 2 year fixed rate mortgage in June 2023 was 5.26%. By comparison, the average 2 year fixed rate mortgage in June 2025 is 4.71%.

Here’s how much you’ll pay at these rates in the initial term if you borrow £200,000 over 30 years:

| Mortgage payment at June 2023’s average rate of 5.26% | Mortgage payment at June 2025’s average rate of 4.71% | Monthly saving if you remortgage |

| £1,106 | £1,038 | £68 |

Use our mortgage cost calculator to work out the cost of your mortgage at different rates.

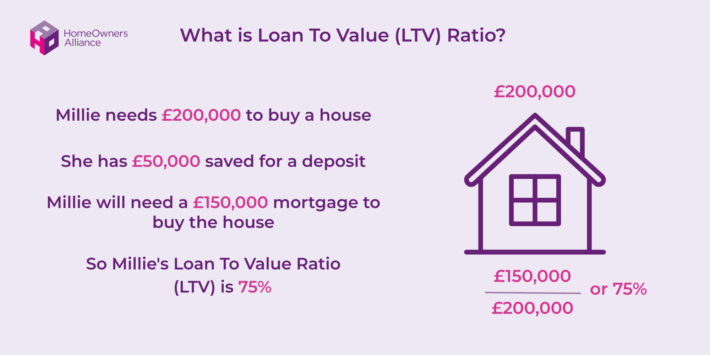

Remortgaging when your house value has increased means you may get access to better rates compared to other deals currently on the market. When you remortgage, the rates you’ll be able to access depend on the LTV – this stands for loan-to-value, and tells you what percentage of the home’s value is borrowed.

So if your house increases in value you’ll own a larger proportion of it. Plus, if you’ve taken out a repayment mortgage, you will have built up equity in it via your repayments too.

In June 2025, the best remortgage rate on a 5 year fixed rate at 90% LTV is 4.38%, while at 80% LTV the best remortgage rate available on a 5 year fixed deal is 4.24%.

If your current mortgage deal ends in the next 6 months, and certainly if it ends in the next 4 months, you should start the remortgage process now instead of waiting in case mortgage rates go down.

By locking in a rate now you can keep it under review to see if a better deal comes up before you switch to your new deal. Award-winning mortgage brokers L&C offer this Rate-Check service for free

When you’re considering should I remortgage now? start by checking your mortgage deal. Remind yourself of your current rate, check when that deal ends, and penalties for exiting early – often called early repayment charges – and what mortgage rates

Get fee-free remortgage advice from our partners at L&C. Use the online remortgage finder or speak to an advisor today.

You should fix your mortgage if you want budgeting certainty that the amount you’ll pay each month on your mortgage won’t change. But if you fix your mortgage, while your repayment amounts won’t increase during the term they won’t go down either if the Bank of England cuts the base rate further.

If you’re asking should I remortgage now and want a fixed rate mortgage, you’ll need to decide how long you want to fix for.

Get fee-free remortgage advice from our partners at L&C. Use the online remortgage finder or speak to an advisor today.

When you’re asking should I remortgage now, how do tracker mortgages and discounted variable rate mortgages compare to fixed rate mortgages?

Some variable rate mortgages come with no early repayment charges which means you could switch to a different deal later down the line without having to pay a hefty penalty. For more information read our guide: What type of mortgage should I get?

Yes. You can start the remortgage process now if your current deal ends within the next six months. You can keep the rate you’ve got under review. While some brokers may charge you to re-check the market, mortgage brokers L&C will do this free of charge so you know you’ll get the best rate available at that time.

Yes. There are lots of reasons why you may want to remortgage in the middle of a mortgage deal such as remortgaging to release equity from your home. But whether it’s right for you will depend on your circumstances:

So if you’re asking should I remortgage now? and you’re in the middle of a mortgage deal before you decide, it’s critical to get advice. A broker can help with the calculations involved in switching and your application. They also have access to deals you can’t get by going directly to the lender and can find the right deal for your circumstances.

Get fee-free remortgage advice from our partners at L&C. Use the online remortgage finder or speak to an advisor today.

In most cases, moving to your lender’s standard variable rate isn’t advisable because they can be extremely expensive and you may be able to save by remortgaging onto a better deal.

However, an SVR mortgage might be a good solution for some, for example, if you have a small mortgage. But if you’re asking ‘Should I remortgage now?’, don’t assume what the best option will be. Always speak to a fee-free broker to make sure you’re on the best deal for you.

Apart from saving money, there are lots of other reasons you may ask ‘should I remortgage now?’

If you’re asking ‘Should I remortgage now’, you’ll also need to make sure you’re in good financial shape before you apply to remortgage. This includes checking your credit rating and taking steps to improve it if necessary, staying out of your overdraft and paying all your bills on time. Find more tips in our guide How to get a mortgage in 6 easy steps.

There are some circumstances which mean remortgaging is unlikely to be a good option such as:

If you’re asking should I remortgage now, you may be considering switching to an interest-only mortgage. If so you’ll need to consider:

If you’re asking should I remortgage now you’ll want to know how much you’ll be able to borrow and what deals are available. To get an idea in a matter of minutes use this remortgage calculator provided by award-winning mortgage brokers L&C.

If you can afford it, paying off your mortgage may be the best option for you. But there are pros and cons to consider. For more information read our guide Should I pay off my mortgage.

HomeOwners Alliance Ltd is registered in England, company number 07861605. Information provided on HomeOwners Alliance is not intended as a recommendation or financial advice.

Mortgage service provided by London & Country Mortgages (L&C), Unit 26 (2.06), Newark Works, 2 Foundry Lane, Bath BA2 3GZ, authorised and regulated by the Financial Conduct Authority (FRN: 143002). The FCA does not regulate most Buy to Let mortgages. Your home or property may be repossessed if you do not keep up repayments on your mortgage.

HomeOwners Alliance Ltd is an Introducer Appointed Representative (IAR) of LifeSearch Limited, an Appointed Representative of LifeSearch Partners Ltd, authorised and regulated by the Financial Conduct Authority. (FRN: 656479).

Independent Financial Adviser service is provided by Unbiased, who match you to a fully regulated, independent financial adviser, with no charge to you for the referral.

Bridging Loan and specialist lending service provided by Chartwell Funding Limited, registered office 5 Badminton Court, Station Road, Yate, Bristol, BS37 5HZ, authorised and regulated by the Financial Conduct Authority (FRN: 458223). Your property may be repossessed if you do not keep up repayments on a mortgage or any debt secured on it.